QUESTIONABLE (at best) June 2025 Employment Report Data from the BLS

Less and Less Credibility to Headline Unemployment Rate and Labor Data

As I mentioned last month on June 8, following the Bureau of Labor Statistics (BLS) monthly employment report for May 2025, the usefulness of any single government report on economic trends is specious at BEST. Today, once again, a discerning review of the BLS data, this time for the month of June 2025, suggests the reported BLS data warrants more than a “grain of salt.” I think any market pundit characterization of the data as “strong” or even as “good” is inaccurate and misleading. So what? So I maintain the Fed needs to start lowering its lending rate sooner-rather-than-later. Whether it does or not, I think the direction of appropriate monetary policy changes is clear, and any delay will probably require an even more intense rate-lowering trend than otherwise. This outlook, if correct, is quite positive for gold price prospects, and I remain heavily invested in gold and related investments.

There really is little, if any, news of economic strength in the Thursday, July 3, monthly employment report from the Bureau of Labor Statistics (BLS). Yet, in response to the report, U.S. Treasury bond yields rose and equity markets traded positively, implying some “risk-on” behavior. Here is a rundown of some of the data in the monthly employment report:

perhaps the main positive is that the already-reported April 2025 and May 2025 reports were revised slightly upward, unlike the downward revisions to the March 2025 and April 2025 in early June 2025;

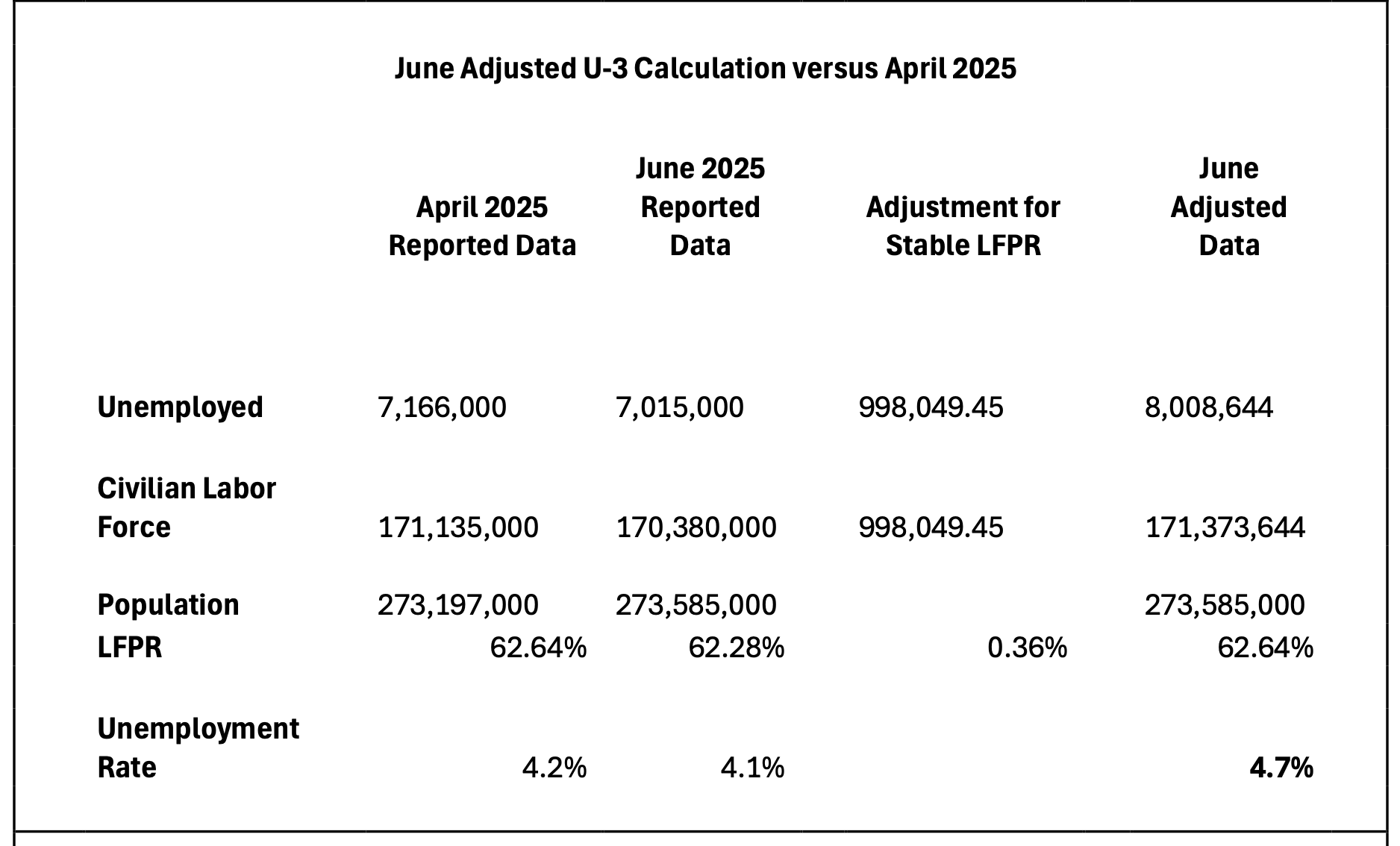

the June unemployment level was reported at 4.1%, slightly down from 4.2% for May, BUT the just-reported June 2025 employment report also indicated approximately 130,000 more people were not in the labor force in June than were in the labor force in May, following that approximately 600,000 more people were not in the labor force in May than were in the labor force in April - if those 730,000 are added back into the labor force and into the unemployment count (comparing June to April), then the June adjusted unemployment rate would be 4.5%; one or two months month does not make a trend, but an 730,000 decline in labor force participation in two months, which suggests a decrease in the Labor Force Participation Rate (LFPR) from 62.6% to 62.0%, seems negative or at least questionable, AND this unemployment level data point had at least SOME impact on economists declaring that the unemployment rate was unchanged from April to May and slightly IMPROVED from May to June;

furthermore, the just-reported June employment data looks even worse when normalized for estimated changes in the LFPR; adjusting for a stable LFPR at 62.6% in June 2025 versus June 2024 and April 2025 suggests an adjusted U-3 (headline) unemployment rate of 4.7% versus the 4.1% reported for June 2025, the 4.2% reported for April 2025 and the 4.1% versus June 2024.

As I mentioned last month, one of my high school Economics classes and I created an unemployment statistical series called “Adjusted U-3” which assumed a steady Labor Force Participation Rate based on long-term trends, and applied the 3-month moving average of unemployment data to that more consistent labor force denominator - the BLS needs such a more credible and useful statistical series - that would provide some needed smoothing, but regarding recent trends would still show a weakening jobs market.